As China’s Communist Party readies for its five-yearly leadership reshuffle, global investors are watching closely to see who will wield power and how they’re poised to manage the world’s second-largest economy as it faces up to its debt dilemma.

When Xi Jinping was settling in as China’s new president in 2013, an animated cartoon presenting his path to power as much more challenging than that of newly re-elected US President Barack Obama went viral.

The message for Chinese viewers was clear: Xi had worked his way through 16 grinding jobs over a 40-year political career, while Obama had somehow emerged as a shooting star from a pugilistic system built on glib speeches and money politics.

Later this year, Xi is set to join an elite group of Chinese Communist leaders who have had the chance to exercise paramount power for at least a decade, while the US is embroiled in speculation about the possible impeachment of President Donald Trump. How Xi’s rise is presented will say much about how he sees his place in the world.

China’s five-yearly transfer of power within the Communist Party – which flows down through the central and provincial government ranks – is due to begin by the middle of October, although it could happen earlier if the opaque power brokers can reach a consensus.

With Xi certain to retain his jobs as party general secretary, state president and head of the military, the main interest will be in which new people in the seven-member Politburo Standing Committee look best qualified – in terms of age, experience and factional ties – to take over as leader in 2022. The transition in the leadership has already been reverberating around the country over the last year, with a major turnover in senior financial regulators and shuffling of political jobs to pave the way for renewal of the roughly 200-member Communist Party Central Committee.

A truly global China

Once Xi has been formally elevated to the status of two-term party leader, he will be able to start comparing his achievements to those of Mao Zedong and Deng Xiaoping. There will be intense interest in how he faces up to mounting economic, demographic and environmental challenges that have at least partly been sidelined as he has been working on strengthening his political base.

“This is the first party congress of a truly globalised China,” says British academic Kerry Brown, who argues that, for the first time, Xi and the other power brokers have to take account of how an uncertain world will view the regime’s new look.

A year ago, Brown says, Xi might have been inclined to throw his weight around and ignore conventions on matters such as retirement age or the need for a potential succession plan. But now, amid rising global economic and political uncertainty, he will see a need and value in projecting a more calm and conventional approach.

Linda Jakobson, chief executive of the Sydney-based public policy initiative China Matters, predicts this 19th Congress will be relatively smooth, compared with the delayed 2012 Congress, from which Xi emerged as leader after an unusually bitter public brawl with a populist regional rival, Chongqing party chief Bo Xilai.

“There’s nothing that big on the horizon,” she says, but warns that, below the veneer of calm, even seemingly all-powerful modern Chinese leaders like Xi are consumed by a sense of “existential anxiety”. Despite their success over the last 35 years, she says, China’s top leaders are “incredibly insecure” about how best to ensure the Communist Party stays in power. This insecurity may well become even more all-consuming during Xi’s next five-year term, as the Communist Party contemplates its 100th anniversary in 2021.

Regardless of the new top leadership’s makeup, it will inherit a wide-ranging and sophisticated economic and public-sector reform program that was set out in 2013 but has been only modestly implemented, as Xi has concentrated on reinforcing his power, cracking down on corruption and pursuing a more assertive foreign policy.

How the new leadership takes up the 2013 Third Plenum recommendations on issues such as state enterprise privatisation and the role of markets has become more critical for the Australian funds management industry with the recent decision to include Chinese shares in the Morgan Stanley Capital Index benchmark for emerging markets.

Australian fund managers have, until now, tended to focus more on Australian assets with exposure to China or the impact of Chinese actions on global markets, rather than on direct investment in Chinese assets. However, in June, MSCI decided to add the shares of 222 Chinese companies to its emerging markets index gradually, after rejecting them three times before because of limitations on capital movement and opaque regulation.

The country’s largest industry fund, AustralianSuper, has played a pioneering role in focusing on the rise of China. The fund opened a small Beijing office and appointed Stephen Joske as a China-based senior manager in 2012. That job is more about analysing China’s role in global markets than direct investment. But, as a director of another major industry fund told Investment Magazine, the long-mooted MSCI change will force funds to take a more formal position on whether and how much to seek direct exposure to Chinese assets.

“Now, if you are in a leadership position in a fund, you need to think about what is happening in China,” says the director, who did not wish to be named. “The Australian economy and what’s happening in China was always there on our agenda. But I would now expect to see more visits by global equity teams.”

Potential debt bomb

Another superannuation fund representative says the industry is underexposed to China but still cautious about direct exposure there because of debt concerns.

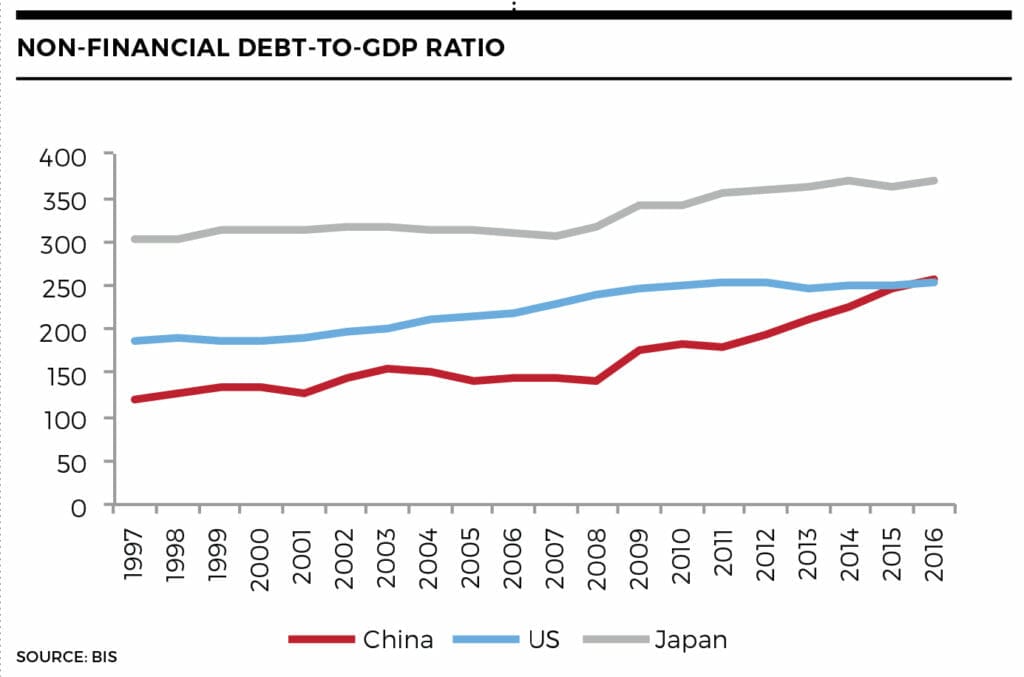

In May, ratings agency Moody’s Investors Service bluntly defined the long-term economic challenge facing the incoming new leadership by cutting China’s sovereign debt rating to A1, due to concerns about the country’s rising debt burden.

“While ongoing progress on reform is likely to transform the economy and financial system over time, it is not likely to prevent a further material rise in economy-wide debt,” Moody’s said at the time, warning about the economy’s dependence on stimulus measures.

Many Western economists based in China say that while Xi came to office amid expectations he would be an economic reformer, he has now locked himself into unrealistically high growth rates and maintenance of a large state-owned enterprise sector, which means debt levels will continue to rise. This is one of the biggest challenges facing the regime. In June 2017, China’s debt surpassed 300 per cent of GDP, certain analysts say.

Some economists interviewed for this article believe the current rate of credit creation can be sustained for only about three to five years, which means a severe credit crunch will probably be one of the biggest challenges for the new leadership. Business advisory firm IMA-Asia noted in a recent outlook: “Since China’s massive debt-fuelled investment binge in 2008-09, it has become clear that the gains from its old growth model, which favoured investment and exports over household consumption, are diminishing. The rising credit intensity of growth and rapid build-up of debt are significant threats to the economy, should Beijing continue to resist slower growth.”

Those expecting some form of credit crunch within a few years tend to think that after enforcing a more authoritarian political environment in his first term, Xi is unlikely to be able to shift back to more liberal economic policies in his second term.

Other, more optimistic, observers say Xi’s flagship anti-corruption campaign, which has both rooted out enemies and restored some moral authority for the Communist Party, may now become less intense, allowing more focus on economic reform. UBS economist Tao Wang expects “improved policy implementation and co-ordination but not drastic changes in policy priority or direction”.

National School of Development economist Yiping Huang wrote after the Moody’s decision that it highlighted past problems, rather than future risks, because the government was taking decisive steps to deal with debt. China Matters’ Jakobson says: “If Xi gets his own people appointed, he could well start genuinely reforming because he understands that is what is needed to keep the economy going. He wants to go down in history as a transformative leader.”

Experienced hands

Close observers of Chinese politics say up to 10 members of the current 25-member Politburo could win one of the four to five spots likely to be vacant on the Standing Committee and be seen as future leaders.

Jakobson says Xi may not show his hand on a succession strategy but if he does, there will probably be two competing candidates.

“A lot can happen in five years,” she says, recalling the way former President Jiang Zemin emerged suddenly, from relative obscurity, after the 1989 Tiananmen crisis, to become China’s senior leader.

Boston University professor Joseph Fewsmith says a key thing to watch at this Congress will be how Xi somehow paves a pathway to continuing to exercise power after his two five-year presidential terms end in 2022. Fewsmith predicts that Xi will try to write himself and his philosophy into the party constitution, to give himself a status similar to Mao’s and Deng’s.

“He could continue to be the central force for 10-15 years without any problem,” Fewsmith says.

But Brown says the most interesting thing to watch at this Congress will be how the Communist Party demonstrates it is responsive to public concerns despite the increasing centralisation of power around Xi.

“The Communist Party wants people to participate at all levels of government, just not through voting,” says Brown, who was director of Sydney University’s China Studies Centre and is now professor of Chinese studies at London’s King’s College. “The leadership is…responding to the people without multi-party democracy. That’s the story of the Congress that probably won’t be recognised outside China.”

That 2013 animated ode to Xi made a big deal about how his long training in city and provincial posts contrasted with Obama’s lack of previous executive administration experience. This is one of the little-appreciated strengths of the Chinese political system; while leaders go through an opaque selection process, they can be better prepared for government administration than many new Western leaders.

Case in point, one of the youngest, most widely touted potential appointees to the Politburo’s Standing Committee, and a potential future leader, is Hu Chunhua. At the age of 54, he has worked as an administrator in Tibet, was China’s youngest ever governor in Hebei province 10 years ago, was then party secretary in Inner Mongolia and is now party secretary in Guangdong province, one of the country’s richest areas. This is the sort of administrative track record that will now be examined intensely around the world when the first Communist Party Congress of global China ends.

This article first appeared in the August 2017 print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.