The inaugural Investment Magazine retail super salary snapshot highlights how hard it is to determine what individuals managing superannuation money in the country’s biggest bank-owned funds are paid. Even so, it is clear they tend to earn more than their industry-fund peers.

Retail super fund executives are overpaid, underperform and put the best interests of shareholders before those of fund members – so the line of the industry fund lobby goes. But is that a fair characterisation?

The inaugural Investment Magazine Retail Super Salary Snapshot attempts to penetrate the rhetoric to examine how the executive remuneration policies at the country’s biggest retail super funds compare with those in the industry fund sector.

It’s no easy task. The complex, vertically integrated corporate structures of retail wealth-management firms, and inconsistent disclosure formats, make it impossible to get a like-for-like comparison on pay policies across the broader super sector.

Since July 1, 2014, all superannuation funds regulated by the Australian Prudential Regulation Authority (APRA) have been required to disclose executive and director remuneration, under the Superannuation Industry Supervision (SIS) Act section 29QB.

For the last three years, the annual Investment Magazine Salary Survey has combed those disclosures to determine the highest-paid chief executives, chief investment officers and chairs across the super industry.

However, this research has only ever painted half the picture.

This is because the disclosure requirements of the SIS Act do not apply to any salaries the parent entities of retail super funds pay.

In most cases, only partial remuneration disclosures are made relating to retail super executives and chairs, and in some cases there are no related pay disclosures at all.

So retail super chiefs on multimillion-dollar salaries, often double what their industry fund counterparts earn, have never appeared atop Investment Magazine’s annual survey.

Another big stumbling block when it comes to comparing the executive remuneration policies of the industry and retail fund sectors is that none of the big five retail players has a dedicated chief executive or chief investment officer for their superannuation business.

In each case, the key roles with responsibility for superannuation clients are tangled up with other parts of the wealth-management business, and often multiple executives have intersecting areas of responsibility.

“In this [regulatory] regime, trying to compare remuneration between sectors is like comparing apples with fish. It’s not even apples with oranges,” professional director Anne Ward says.

Ward is the chair of Commonwealth Bank’s three superannuation trustees and also chair of one of the country’s biggest corporate funds, Qantas Super. She also regularly chairs the remuneration committees of those funds, giving her a unique insight into the differences in pay structures across the broader industry.

For the external observer, accountability around pay is also harder to track in retail super players, because of their vertically integrated business models. Each of the big five retail super trustees has a number of business relationships with other arms of their parent company. Typical related-party transactions that retail super funds participate in include funds management mandates, cash and currency management, group insurance, and administration services.

Proponents of the vertically integrated model argue benefits can flow from investing through related parties, such as reduced transactional activity and associated costs, the negotiation of better terms, greater efficiencies, better access to information and more control over governance. But both APRA and the Australian Securities and Investments Commission (ASIC) have voiced concerns about how the industry is managing potential conflicts of interest in these relationships.

Inside the big five

The inaugural Investment Magazine Retail Super Salary Snapshot focuses on the five biggest players in the retail superannuation sector: AMP, National Australia Bank, Westpac Banking Corp, Commonwealth Bank of Australia (CBA), and ANZ Banking Group.

Between them, AMP and the big four banks, which all operate under vertically integrated business models, have more than $400 billion of the $570 billion retail superannuation market. And they are all hungry to win a bigger slice of the $2.2 trillion super pool by convincing more customers from other parts of their businesses, such as banking and life insurance, to roll over their compulsory retirement savings.

The diagrams accompanying this article aim to depict the web of commercial relationships between related parties affecting superannuation assets within these five biggest players, while noting any disclosed remuneration relating to superannuation duties of chairs and other individuals with responsibilities comparable to that of a super fund chief executive or chief investment officer.

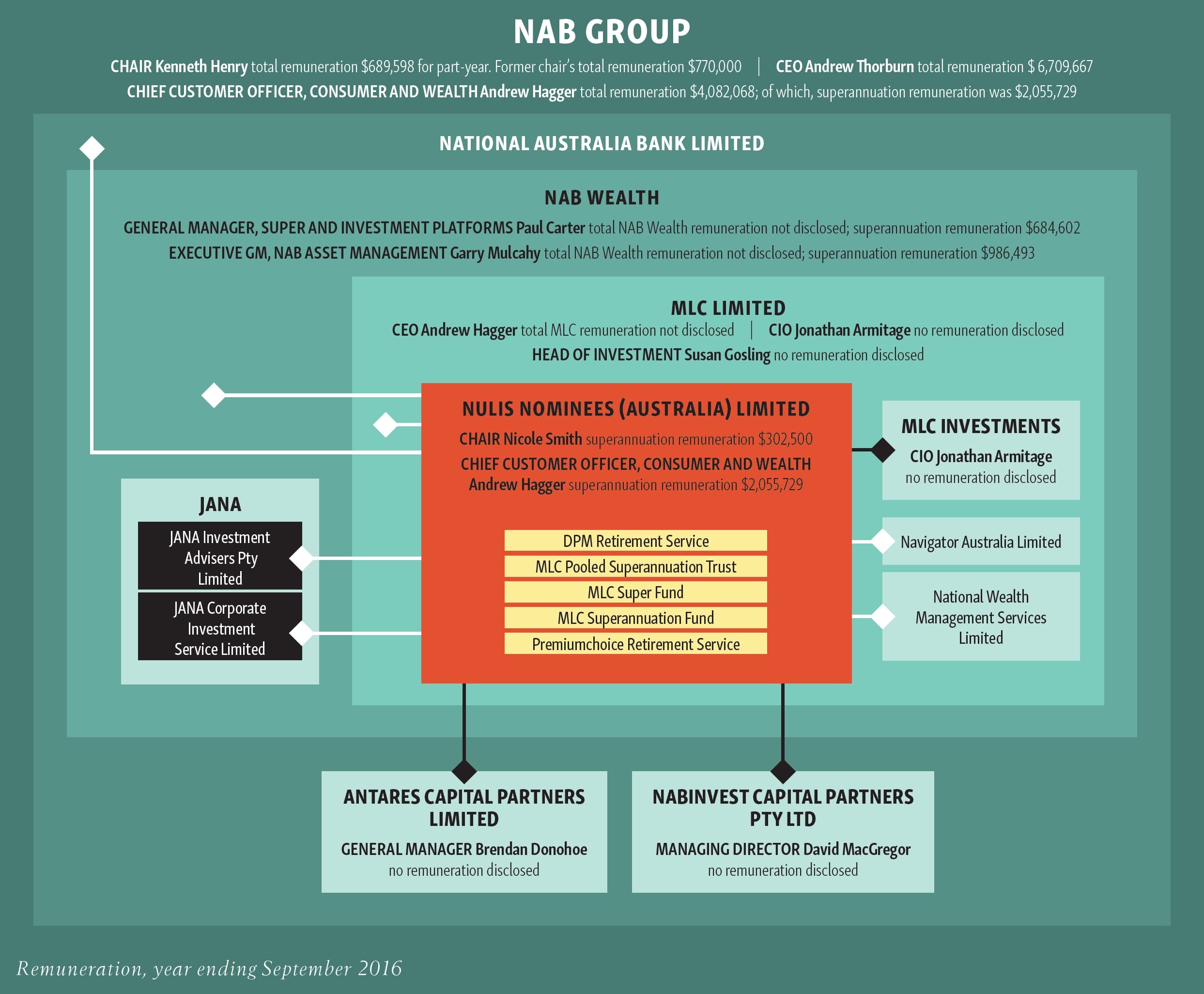

National Australia Bank

In the year to September 2016, National Australia Bank spent a total of $9.1 million on director and executive remuneration in relation to its superannuation businesses.

That’s roughly 54 per cent more than the $5.9 million bill for director and executive remuneration at the country’s largest industry super fund, AustralianSuper, in the comparable financial year. Both AustralianSuper and NAB’s MLC Super have about $109 billion under management.

At NAB, more than $2 million of super related remuneration went to one individual – group chief customer officer, consumer and wealth, Andrew Hagger. His total remuneration, including his broader duties outside of superannuation, came to nearly $4.1 million.

In comparison, AustralianSuper chief executive Ian Silk earned total remuneration of $798,186, while the fund’s chief investment officer and deputy chief executive, Mark Delaney, out-earned his boss, after qualifying for a $548,207 bonus to bring his total annual remuneration to just under $1.24 million.

Total annual remuneration for NAB asset management executive general manager and acting executive general manager, wealth products, Garry Mulcahy, is unknown; however, it was disclosed that he received $986,493 for his duties related to superannuation. Within the NAB-owned wealth-management business MLC Ltd sit chief investment officer Jonathan Armitage and head of investments Susan Gosling but no remuneration is disclosed for either of them.

Not only do retail super funds tend to pay their executives more for equivalent roles, they also tend to have more layers of highly paid executives. For example, MLC is a part of NAB Wealth, which has its own senior executive team. NAB Wealth executive manager super and investment platforms, Paul Carter, was paid $684,602 last financial year for his super duties. Carter’s total remuneration for the period is unknown.

Not only do retail super funds tend to pay their executives more for equivalent roles, they also tend to have more layers of highly paid executives. For example, MLC is a part of NAB Wealth, which has its own senior executive team. NAB Wealth executive manager super and investment platforms, Paul Carter, was paid $684,602 last financial year for his super duties. Carter’s total remuneration for the period is unknown.

As for trustees in NAB’s superannuation business, Nicole Smith – the chair of NULIS Nominees, the trustee for MLC’s five super funds – received $302,500 for her duties, making her the highest-paid super fund chair in the country. In comparison, AustralianSuper’s Heather Ridout earned $187,355.

NAB restructured its wealth-management division in late 2016, following the sale of 80 per cent of the group’s life insurance business to Japan’s Nippon Life.

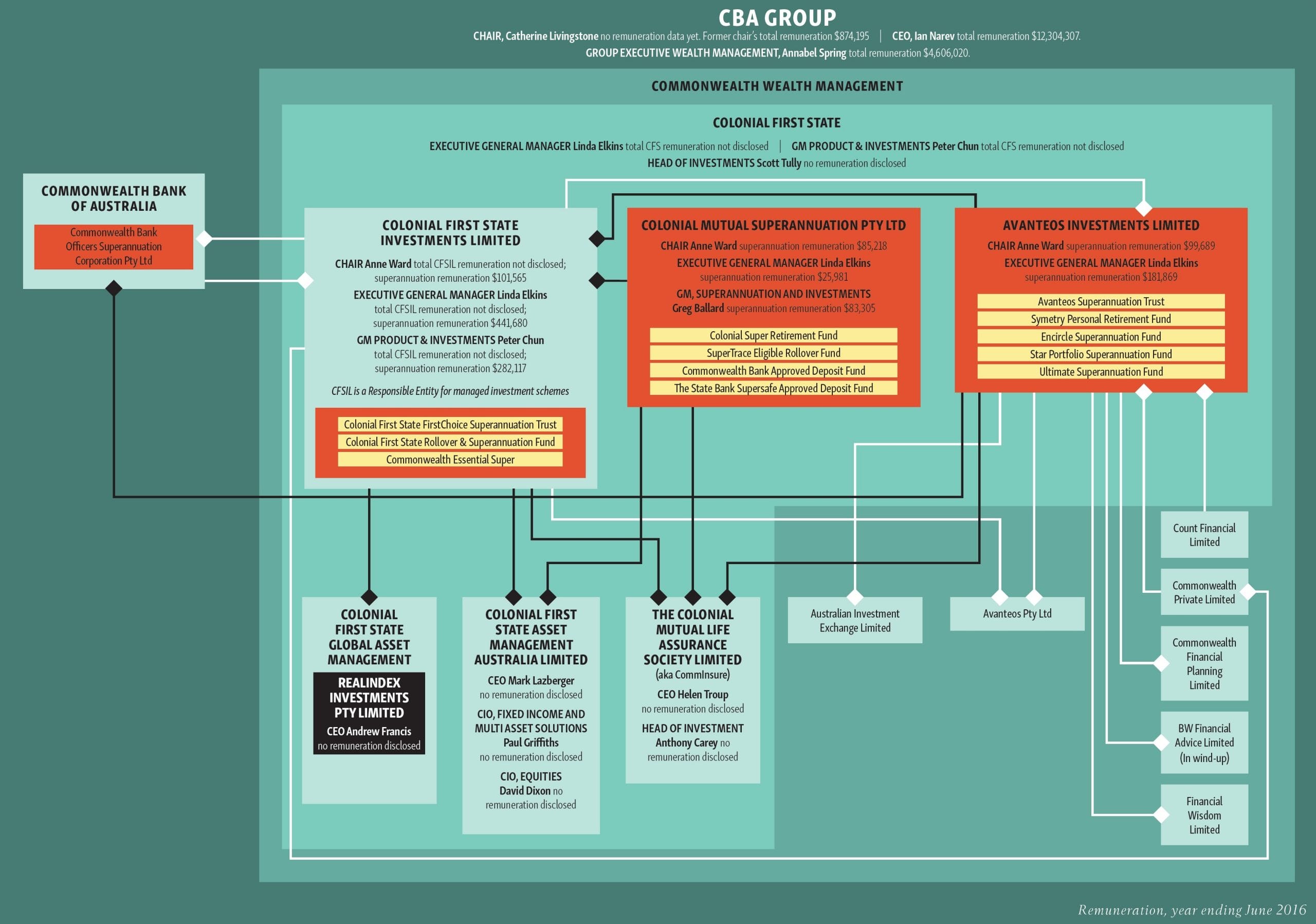

CBA Group

The country’s biggest bank, CBA Group, paid its group executive, wealth management, Annabel Spring, more than $4.6 million in the financial year ended June 2016. It is not known how much of this is linked to Spring’s oversight of the banking giant’s superannuation businesses.

Sitting within CBA’s wealth management business that reports to Spring is Colonial First State (CFS), which includes three separate super trustees with responsibility for a dozen super fund businesses.

Separately, CBA has a fourth trustee responsible for its corporate super fund.

Colonial First State executive general manager Linda Elkins was paid $649,530 in relation to her superannuation duties last financial year. Her total remuneration was not disclosed.

The remuneration for Colonial First State head of investments Scott Tully is not disclosed.

Other highly paid super executives within the group include Colonial First State Investments general manager, product and investments, Peter Chun, who pockets $282,117 for his super-related duties.

Chun’s total remuneration is unknown.

Colonial Mutual Superannuation general manager superannuation and investments, Greg Ballard, received $83,305 for his super related duties.

“I don’t think there are any staff in management who you could say work solely in relation to one super fund,” says Ward, who chairs three of CBA’s super trustees.

“They all have roles that span a range of activities, as do the board members.”

Last financial year, Ward received $266,472 for her super fund duties.

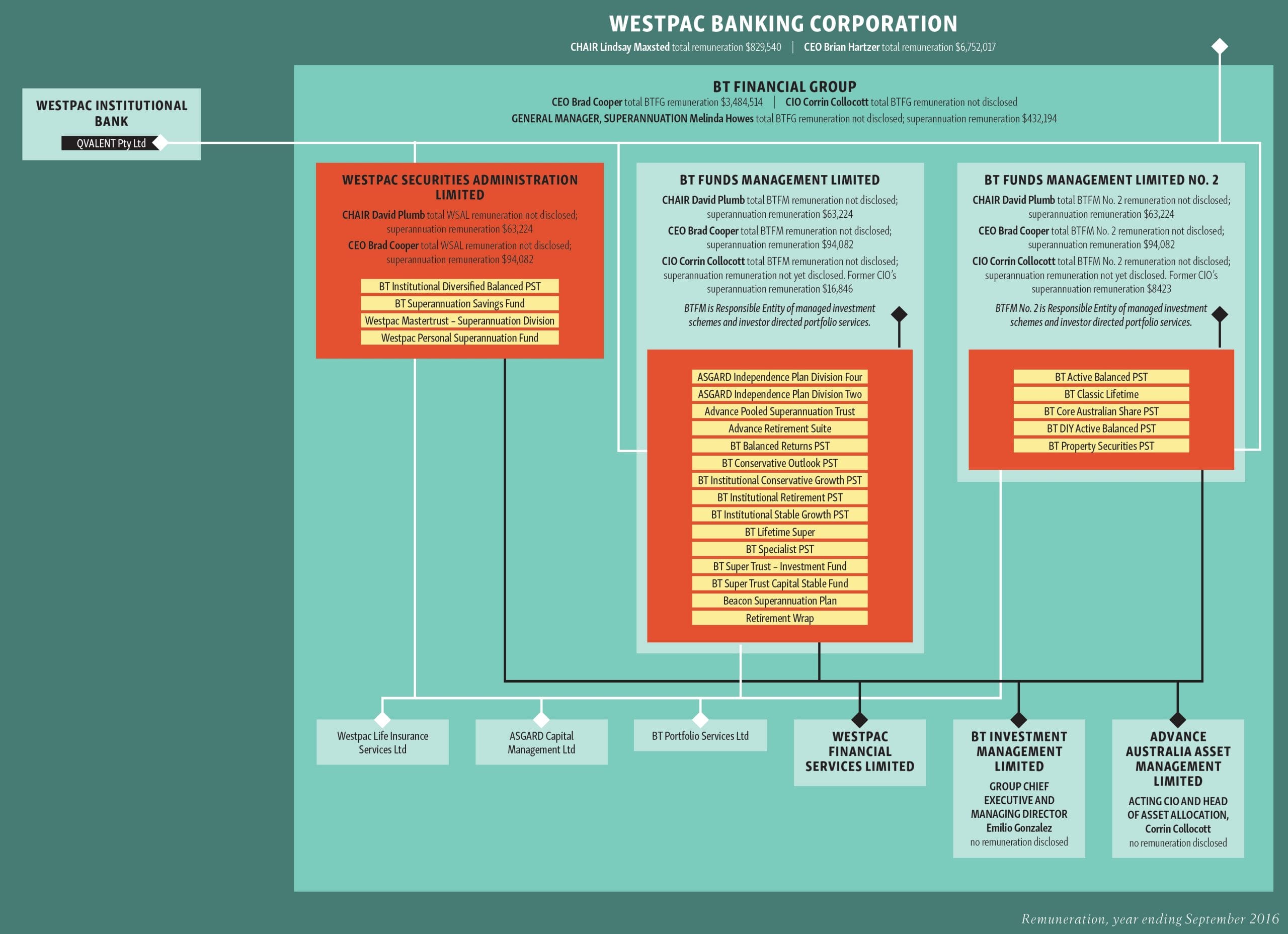

Westpac Banking Corp

BT Financial Group, the wealth-management arm of Westpac Banking Corp, houses three separate superannuation trustees that run a total of two dozen super products, including wrap platforms.

In the financial year ended September 2016, BT Financial Group chief executive Brad Cooper received total remuneration of $3.48 million, of which $282,246 – or 8.1 per cent – was for time spent on superannuation related duties. BT Financial Group general manager, superannuation, Melinda Howes, received $432,194 related to superannuation duties; her total remuneration for the period is unknown.

The three Westpac-owned trustees each paid Cooper $94,082 last financial year, bringing his remuneration related to superannuation duties to $282,246. His total remuneration was not disclosed. BT Funds Management chief investment officer Corrin Collocott was paid just a total of $25,269 by the group’s super trustees.

Collocott’s total remuneration was not disclosed.

BT Financial Group chair David Plumb received $63,224 from each of the three trustees, totalling $189,672.

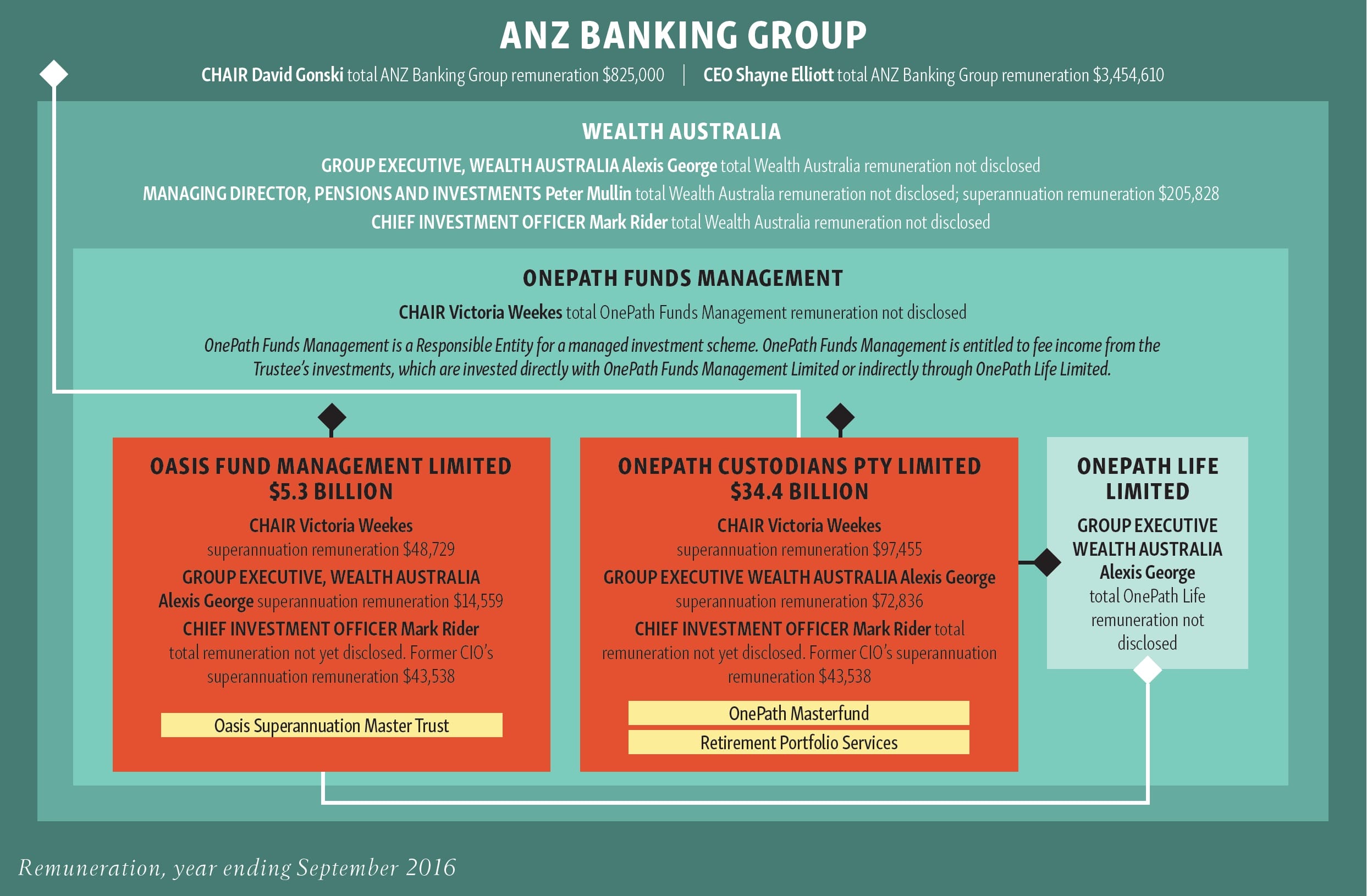

ANZ banking group

As with the rest of the big retail players, there is little transparency on what executives are paid in the superannuation business of ANZ Banking Group.

In the most recently reported financial year, ending September 2016, no pay disclosures were reported for ANZ Wealth Management group executive Alexis George.

ANZ Wealth Management managing director pensions and investments Peter Mullin was paid $205,828 for superannuation-related duties, although his total remuneration is unknown.

ANZ Wealth Management chief investment officer Mark Rider was appointed after the reporting period.

Former ANZ Wealth chief investment officer Stewart Brentnall received $89,076 for his super fund duties during the period; no information was available on his total remuneration either.

Victoria Weekes, who chairs the ANZ Banking Group’s super funds, addressed the topic of related-party transactions.

In addition to arguing they offer benefits, she notes that related-party appointments are not given carte blanche. ANZ’s trustee boards have a comprehensive program of reviewing executive remuneration, along with staff remuneration and incentive programs more broadly, she says.

“That extends to any related-party provider that has a material impact on the superannuation funds, including the funds’ managers, and hence their executive remuneration,” Weekes explains. “Our role in remuneration oversight includes reviewing and approving performance objectives, the remuneration framework and benchmarks, and the recommended performance outcomes and resulting remuneration. This arguably gives us more oversight and control than we have over independent, third-party arrangements.”

She cited a recent decision to outsource the OnePath wrap platform to Macquarie Investment Management as evidence of trustees putting the interests of super fund members first.

Weekes received $146,184 for her duties as chair of the two super fund trustees.

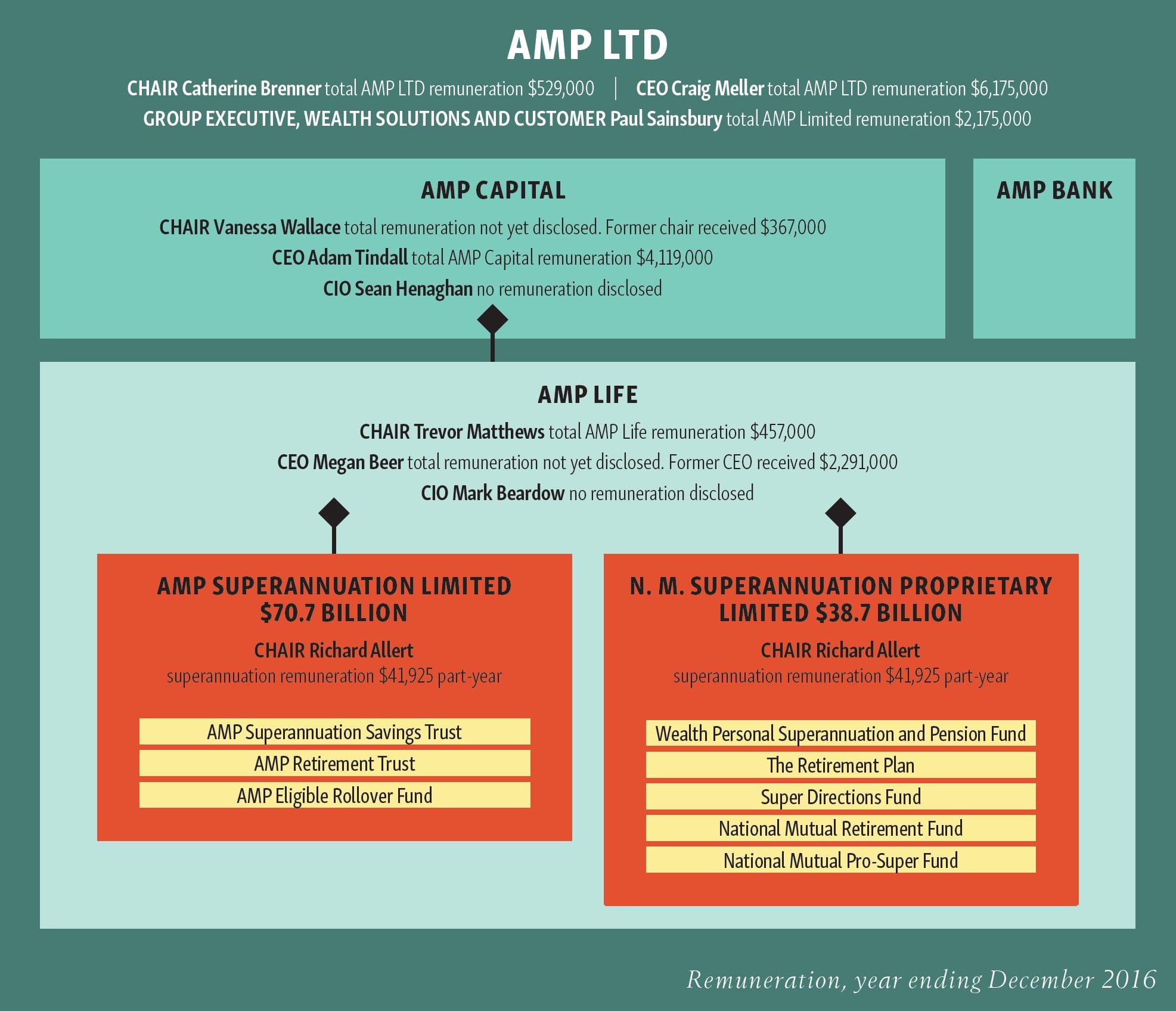

AMP Ltd

AMP Life, the life insurance division of diversified wealth management company AMP Ltd, contains two superannuation trustees that together

run eight super businesses.

AMP Life outsources a substantial set of functions to AMP Capital. This includes investment management of a significant portion of the individual assets and investment options offered through AMP Life.

In the year ended December 2016, AMP Capital chief executive Adam Tindall received total remuneration of $4.12 million, although none of this was reported as related to superannuation duties. No remuneration was disclosed for AMP Capital chief investment officer Sean Henaghan.

The former chief executive of AMP Life received total remuneration of $2.29 million; again, none of this was reported as related to superannuation duties. No remuneration was disclosed for AMP Life chief investment officer Mark Beardow.

AMP Group executive, wealth solutions and customer, Paul Sainsbury, has responsibility for the management of superannuation, retirement and investment platforms. The role is newly created after a leadership restructure in November 2016 and does not yet have remuneration data. For a similar level role in 2016, Sainsbury earned $2.2 million.

He reports to group chief executive Craig Meller, who earned $6.2 million in 2016.

Richard Allert, chair of AMP’s super funds, received $83,850 for super fund duties for his partial year as chair in calendar year 2016.

Follow the money

Despite all the challenges with making direct comparisons, it is clear that senior individuals can typically expect to earn an order of magnitude more working at a retail super fund than at an industry fund.

Rather than a simple game of pay-packet envy, however, the more interesting and important issue is whether the pay deals in the retail super world are structured in a way that adequately protects the interests of consumers by aligning pay incentives with good practice.

CBA’s Ward tells Investment Magazine she is fan of fixed remuneration plus an ‘at-risk’ component, with the latter dependent on performing above expectations. However, she says there is no one remuneration structure to suit every organisation.

“Even within the same sector, you can’t compare remuneration structures because the business model and legal structures are quite [varied],” she says. “For instance, the numbers that have been disclosed for me in relation to Colonial are not comparable to the information disclosed for me in relation to Qantas Super.”

NAB general manager corporate super, Lara Bourguignon, says that since the Future of Financial Advice (FoFA) reforms came into force on July 1, 2013, there have been no sales-based metrics on executives’ scorecards, so she and her colleagues cannot be incentivised to bring in new business.

Bourguignon says: “Our incentives are not linked in any way to sales or retention of members; it is very much focused on having engaged people operating in a climate that manages risk and is focused on lifting capability.”

She says the holy grail of conflict management in NAB’s super business is the roles and responsibilities charter – a tripartite agreement between NAB, the trustee board and the service company.

“Essentially, that agreement makes it very clear that the trustee’s number one responsibility is members’ best interest. Assuming members best interest is satisfied, the trustee needs to manage the commercial arrangements. It’s an ‘and’ not an ‘or’.”

KPMG partner, performance and reward, Tim Nice, says remuneration practices across the retail super sector are “heading towards global best practice”. One of the ways this is being accomplished, he says, is by deferring manager pay, so they are incentivised to consider the wider vision.

“An equity plan may not directly link to the manager’s individual success, but it does keep the focus not just on shareholders, but also on other stakeholders [such as members], because share price reflects a combination of views on an organisation.”

Leave a Comment

You must be logged in to post a comment.